Around 850 million people globally lack any form of digital identification. A large percentage of this population comes from Sub-Saharan Africa and South Asia. This creates challenges, especially in accessing critical services, building robust systems to tackle identity fraud, and promoting financial inclusion. In Nigeria, financial inclusion increased to 74% in 2023, up from 68% in 2020. However, it has failed to hit the 95% long-term target set by the Central Bank of Nigeria (CBN).

The quest for accurate and comprehensive data on key identification systems has become important in Nigeria’s rapidly evolving digital landscape. This article will analyse the enrolment figures for critical identification platforms, shedding light on Bank Verification Number (BVN), National Identification Number (NIN), voter registration, SIM registration, passport issuance, and driver’s license registration.

BVN

In February 2014, the CBN deployed a centralised BVN system with a clear mandate to institute effective Know Your Customer (KYC) standards, provide biometrics solutions for identity management, combat fraud, and promote an efficient payment system. The Nigeria Inter-Bank Settlement System (NIBSS) was tasked with providing the Application Programming Interface (API) for financial institutions to integrate their systems into the BVN database.

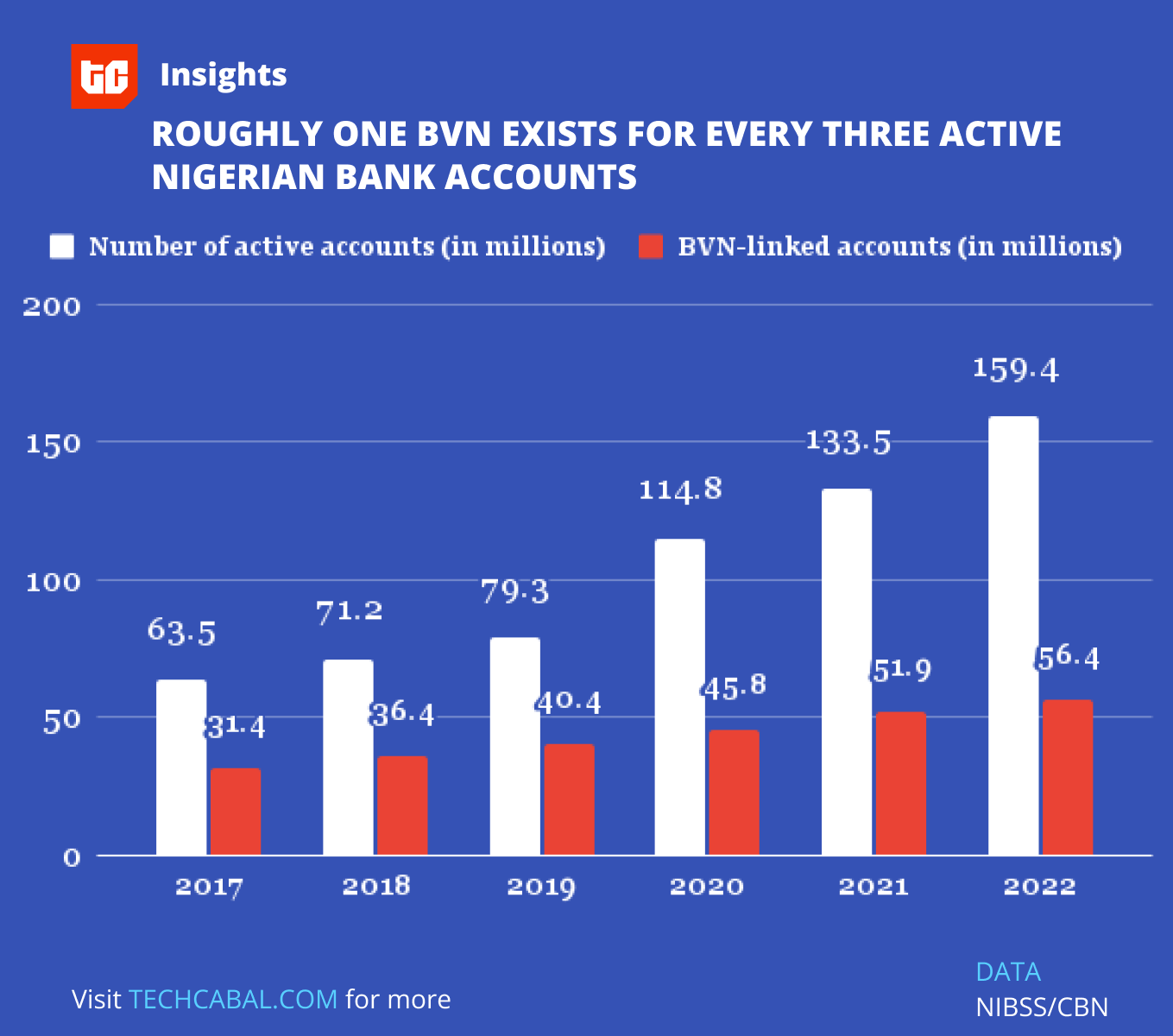

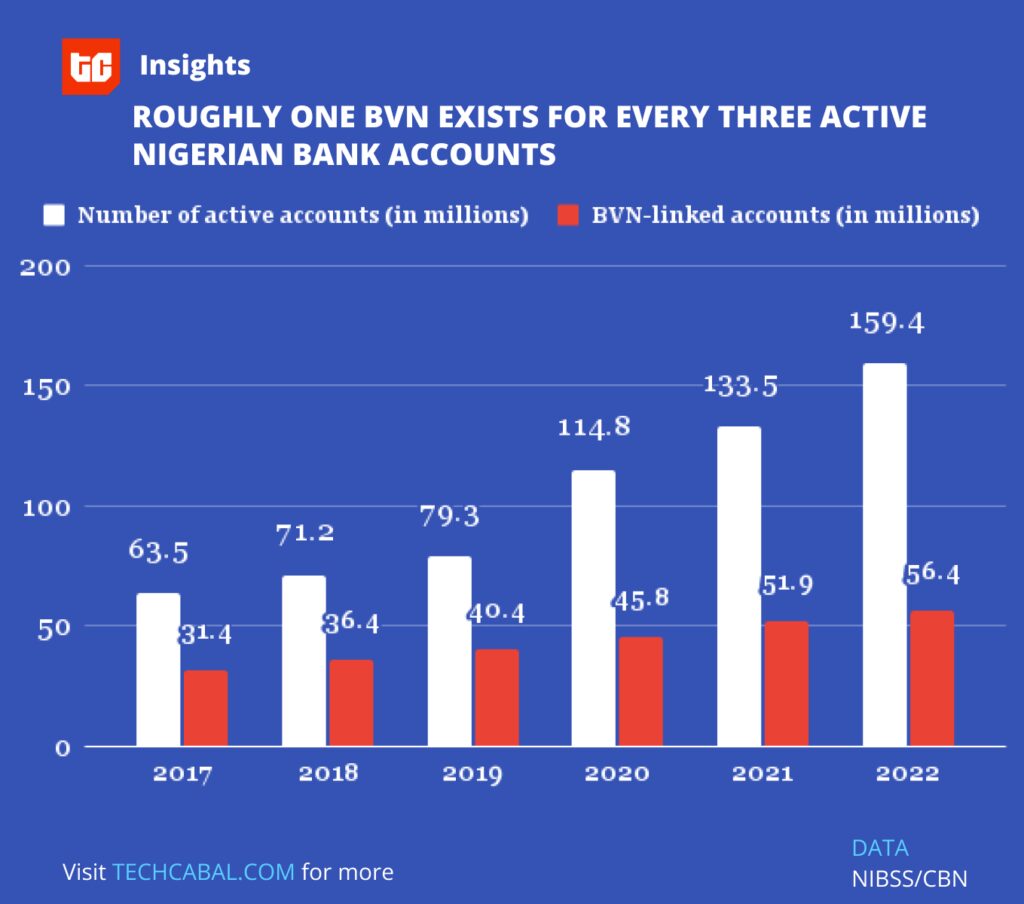

In 2019, the CBN set a five-year target to hit 100 million registered people in the BVN database. As of December 2023, 59,956,056 accounts have been registered, per NIBSS, placing it 40% short of the benchmark. Based on the CBN’s December 2022 Financial Stability Report, there were 159.42 million active customer accounts. 127.92 million of these were linked with BVNs. The gap in the figures is primarily because the CBN’s data includes individuals with multiple accounts, while NIBSS’s is unique.

Notably, there was nearly one BVN for every three active bank accounts in 2022, up from about one in two in 2017. The data suggests the trend will continue to rise.

This disparity benefits payment platforms in the fintech space that allow customers to open wallets and operate them easily, compared with the stringency of creating and maintaining a traditional bank account. However, while introducing the BVN has certainly helped entrench financial inclusion, bad actors have also targeted it.

A study by the Nigerian Financial Intelligence Unit (NFIU) disclosed that between 2015 and Q1 2018, 9,517 suspicious activity reports (SAR) were filed, with 6,503 of them (68.3%) being BVN-related. As of December 2022, 7,399 BVN-linked accounts were placed on a watchlist by the CBN under suspicion of fraudulent activity. Factors attributed as causes include the random issuance of affidavits in place of original documents and insider abuses by financial institutions.

To ramp up the BVN drive in the Nigerian financial system, the CBN has announced that it will freeze accounts not yet linked to BVNs and NINs from April 2024.

NIN

Based on the most recent data from the World Bank, only 42.6% of Nigerians have birth certificates, which speaks to a gap in identity management. In 2020, the World Bank entered into an agreement with Nigeria for the Digital Identification for Development project. Its collaboration with the National Identity Management Commission (NIMC) aimed to capture 148 million Nigerians and provide them with a digital ID by June 2024. The figure represents 65% of the projected population of Nigeria.

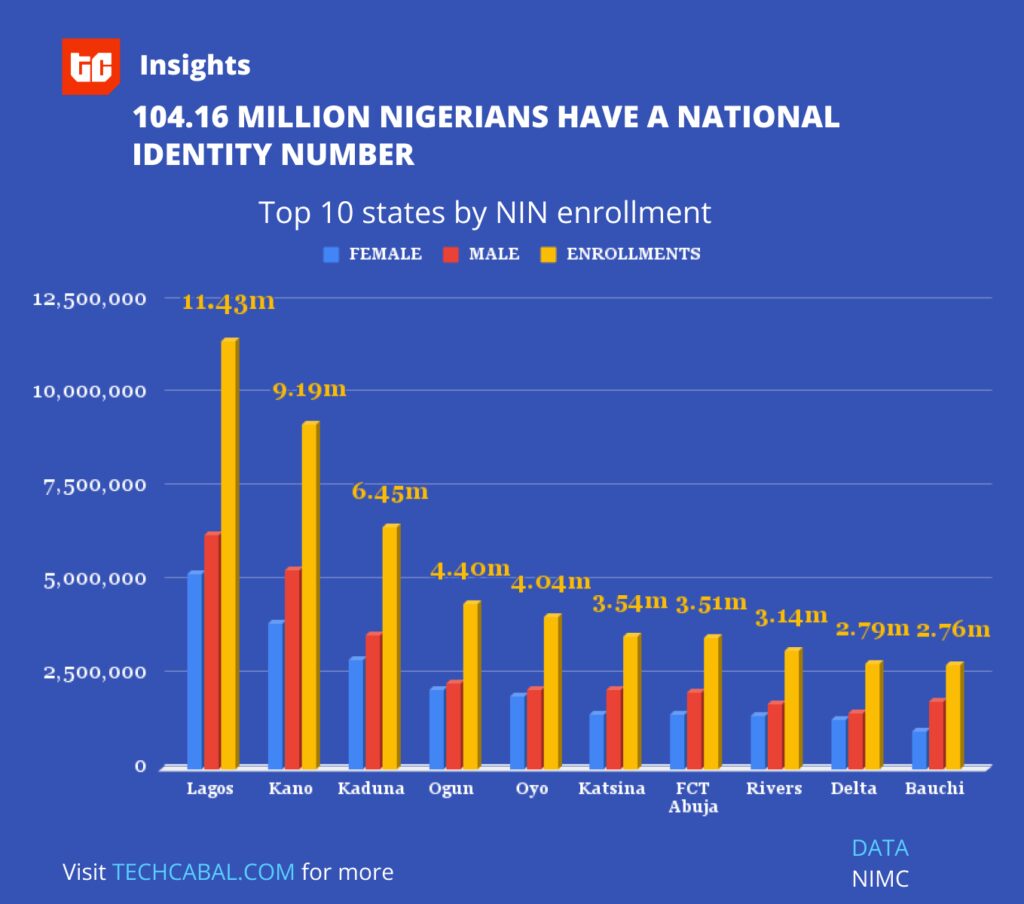

As of December 2023, 104.16 million Nigerians had been issued NINs; 59.12m (56.8%) were male, and 45.04m (43.2%) were female. This marks a 10.77% increase from the 94.03 million registered in 2022 but would almost certainly fall short of the target set for 2024. Lagos, Kano, and Kaduna, with 11,427,825, 9,196,640, and 6,451,081 enrollees, respectively, account for 26% of all NIN registrations.

Voter registration

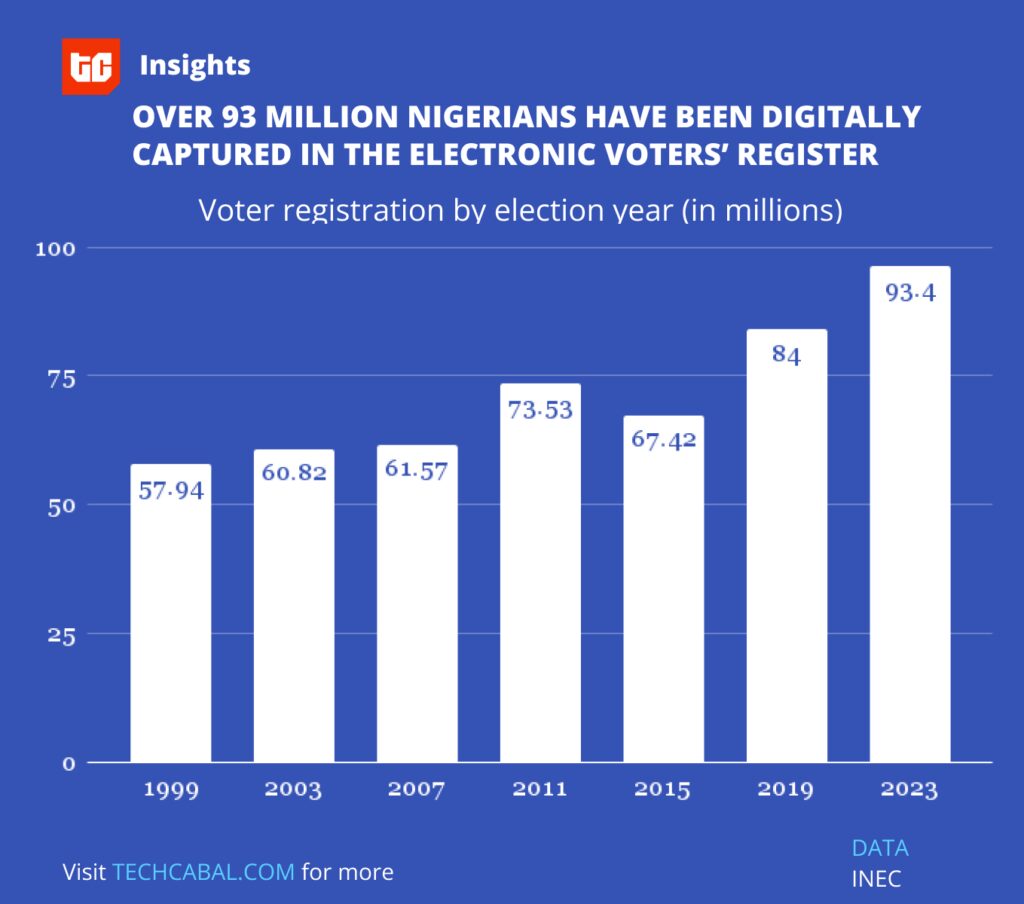

The Independent National Electoral Commission (INEC) began digitising the voter database in 2010 when the Electronic Voters’ Register (EVR) was introduced in preparation for the 2011 general election. Since then, there have been notable technological upgrades, including the Bimodal Voter Accreditation System (BVAS) and INEC’s Results Viewing Portal (IReV). The upgrades were touted to restore trust in the electoral process by eliminating duplication and minimising discrepancies.

While there has been success in integrating biometrics, the jury remains out on how effective this has been. Leading up to the 2023 elections, around 45% of “completed registrations” were deemed invalid by INEC for reasons including incomplete data and complicity by INEC staff in infractions that invalidated the process. During the general elections, the BVAS failed, in some instances, in accrediting voters despite having captured their biodata. Doubts have also been raised about the integrity of the voter register with allegations of underage voters, fake identities, and questions over a historically low turnout of 27% despite a record number of registered voters at 93.4m.

SIM registration

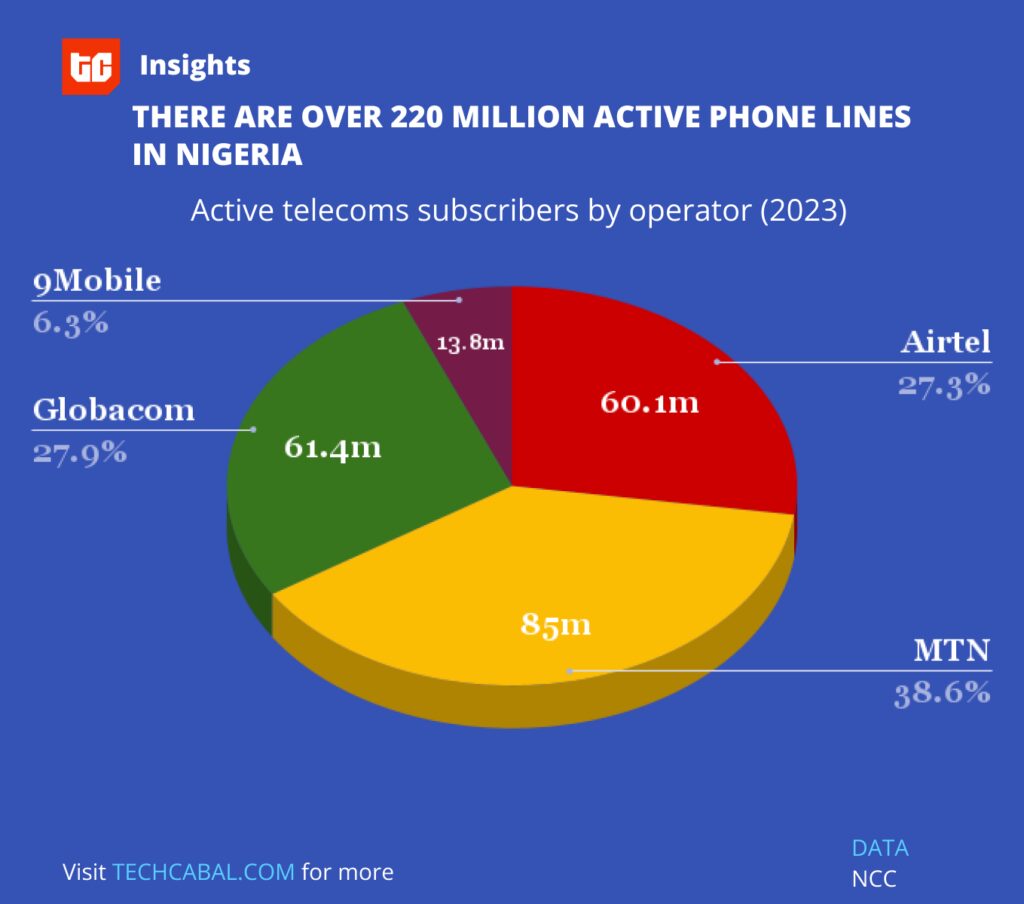

The Nigerian Communications Commission (NCC) is legally mandated to maintain a central database and institute data and confidentiality protection for all telecom subscribers. In 2022, the total number of registered SIM cards crossed 300 million. However, a sizable fraction of those are inactive. As of August 2023, the NCC revealed that there were 220 million active subscribers distributed among four major operators.

An estimated 12.4 million phone lines are yet to be linked to their NINs, prompting the NCC to issue an ultimatum of February 28, 2024, before those lines are barred from placing or receiving calls.

Passport

The biometric passport was first adopted in 2007. Since then, efforts to ensure the collection of passports often take a long waiting time and are encumbered with issues, including a shortage of booklets. Fast-tracking involves high costs and back channels, contributing to a slower adoption rate than other forms of identification.

The latest developments show some promise as e-passport issuance has now been automated after it went live on January 8. A step-by-step guide on how to apply for a passport online can be found here.

However, a publicly available database on passport issuance in Nigeria is hard to come by, and even the most recent report on passport applications from the Nigerian Bureau of Statistics (NBS) dates back to 2018. It disclosed that 1,011,158 passport applications were received in 2018, up from 720,958 in 2017—a 40.25% increase. Recent trends suggest that the demand for passports has not waned. In 2022, the ministry of interior revealed that it had received an unprecedented 750,000 applications in the first five months, issuing 625,000. Overall, around 1.7 million passports were said to have been issued that year, per the ministry.

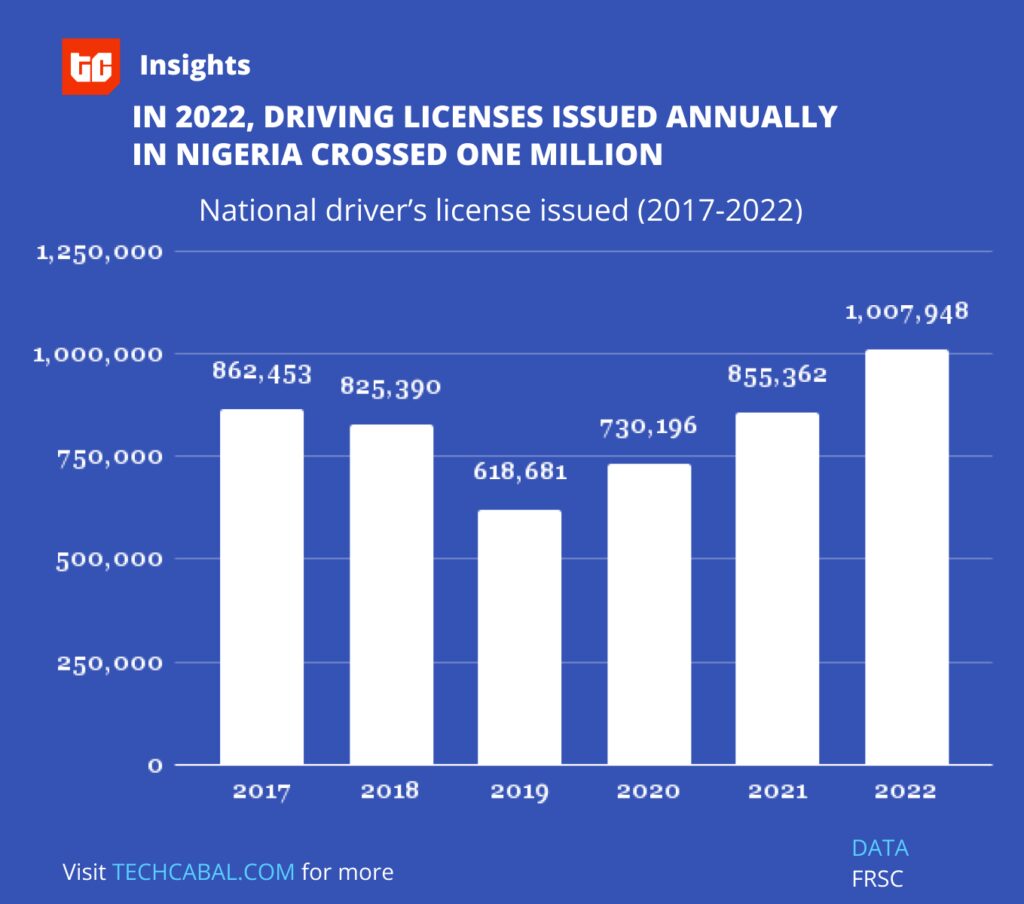

Driver’s license

The harmonisation and digitisation of the driver’s license have undergone various phases since the first national driver’s license (NDL) was produced in 1990. The Federal Road Safety Corp (FRSC) is the agency tasked by law to regulate and digitalise NDLs.

In the early days, NDLs were created using standalone computers that captured biodata. Biometrics were manually placed before the cards were sent to the Nigerian Security Printing and Minting Company Limited for lamination. Over time, the NDLs evolved and assumed more sophistication. The current NDL is the Enhanced National Driver’s License Scheme (ENDLS).

In 2022, NDLs issued crossed one million for the first time, based on FRSC records. As of Q2 2023, the FRSC produced 161,246 NDLs, up from 124,684 in Q1 2023. Nevertheless, the FRSC has disclosed that network bandwidth issues are a major challenge in digitising NDLs. Slow network speeds mean applicants wait unnecessarily long periods to capture their biodata.

In conclusion, Nigeria is on track towards establishing a robust digital identity architecture, with the financial sector as proof of its tangible benefits. The NIN is pivotal in this endeavour, weaving through various applications as the common thread.

More strategic measures can be put in place to optimise the momentum gained so far. These include the consolidation and regular auditing of databases, prioritising outreach efforts in historically disenfranchised rural areas, intensifying educational initiatives to articulate the advantages of digital identities, cultivating a data-driven culture, eliminating regulatory bottlenecks, fostering transparency, and fostering more partnerships—particularly between the government and corporate entities with proven mechanisms for advancing digitisation.

Ultimately, Nigeria’s digital identity will continue to evolve, paving the way for a more inclusive and technologically empowered future.