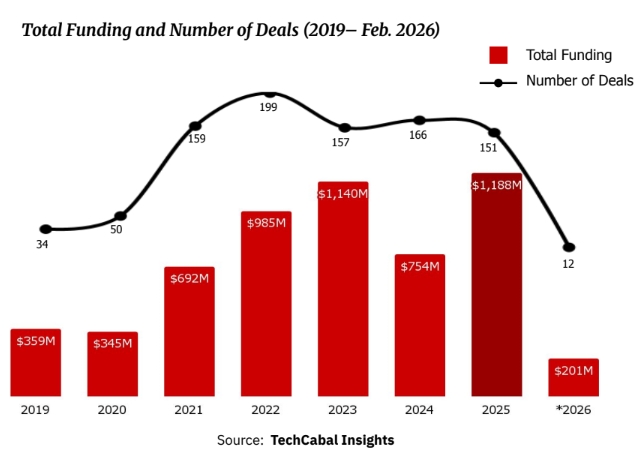

Africa’s climate tech sector has raised $5.66 billion across 928 deals between 2019 and February 2026. But the year-by-year breakdown reveals something more nuanced than a simple growth curve.

Funding more than doubled from $359M in 2019 to $692M in 2021, as global climate finance found its footing in African markets. The sector hit an early peak of $985M in 2022, followed by a dip to $754M in 2024, reflecting broader macro headwinds across emerging markets.

Then came 2025. Climatetech startups raised a record $1.18 billion, a 57% jump over the prior year. Deal volume declined for the third consecutive year, falling to 151 transactions from a peak of 199 in 2022. The apparent contradiction of more money, fewer deals is precisely the story. Capital is consolidating. Investors are writing bigger cheques into fewer, better-proven businesses.

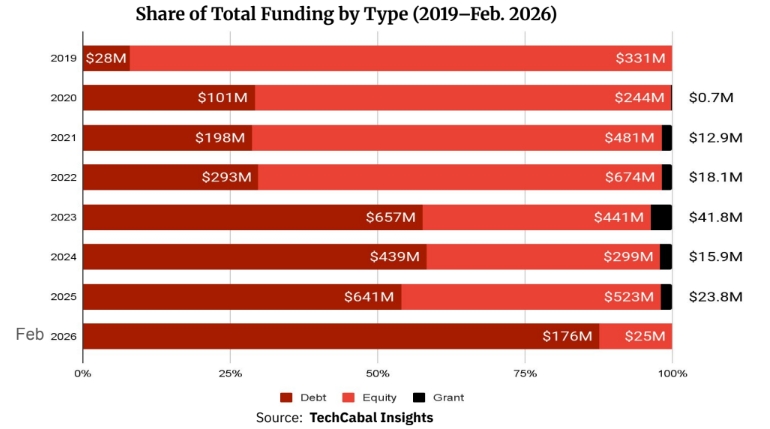

Debt has dethroned equity. Africa’s climate tech is now a credit market

In 2019, debt represented just 8% of total climate tech funding. By 2025, debt had climbed to 54% of all funding, with 23 debt deals raising $641M, outpacing 81 equity rounds by a factor of 2.5x. The shift from 30% in 2022 to 54% in 2025 is not cyclical. It is structural.

Debt is growing because the biggest companies are now mature enough to handle large loans. The sector’s biggest operators Sun King, d.light, M-KOPA are asset-heavy, revenue-generating businesses with predictable receivables from pay-as-you-go consumer models. At their scale, debt is structurally cheaper and less dilutive than equity. They are no longer startup bets; they are infrastructure businesses accessing infrastructure-grade capital.

WHO CAPTURED THE CAPITAL?

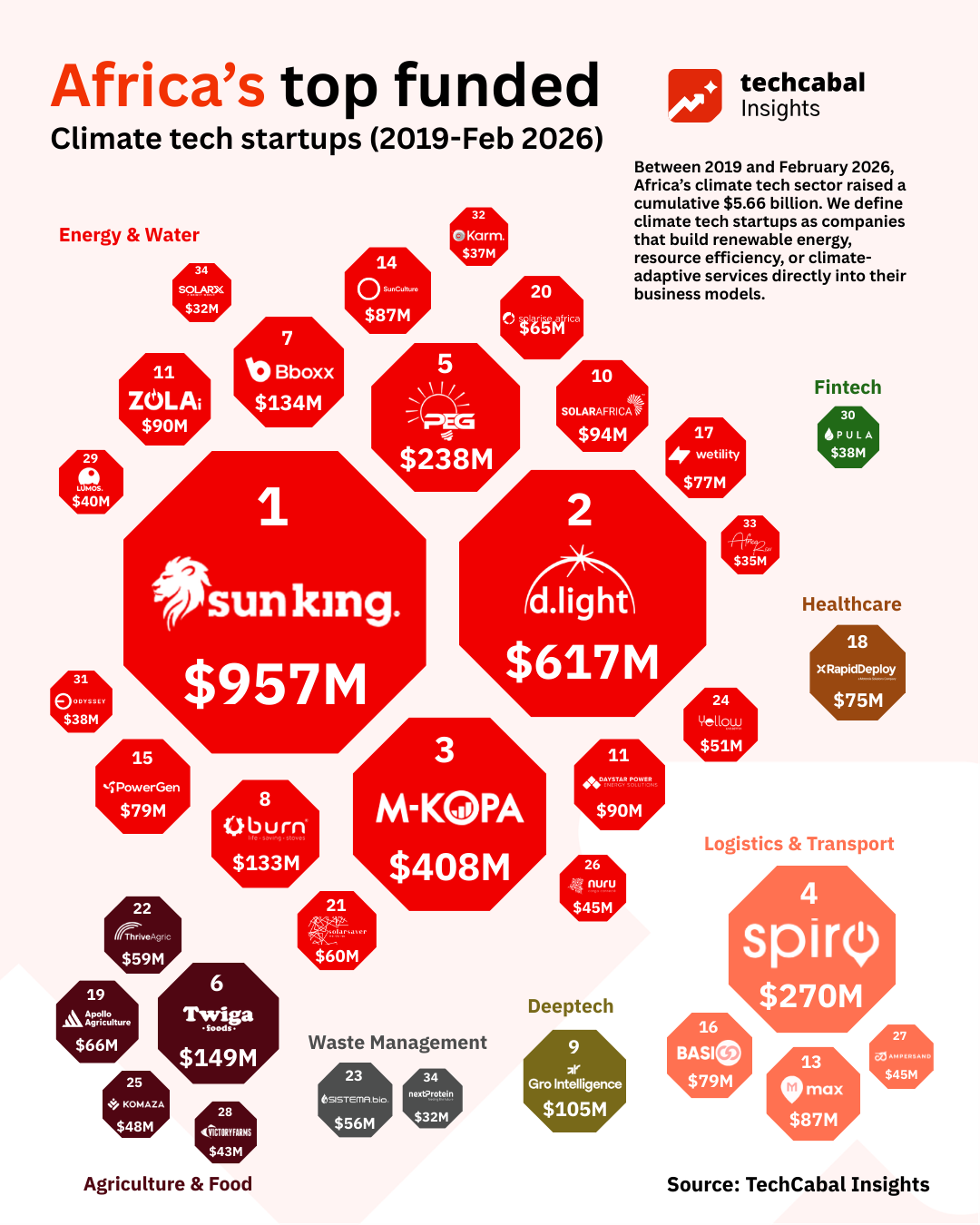

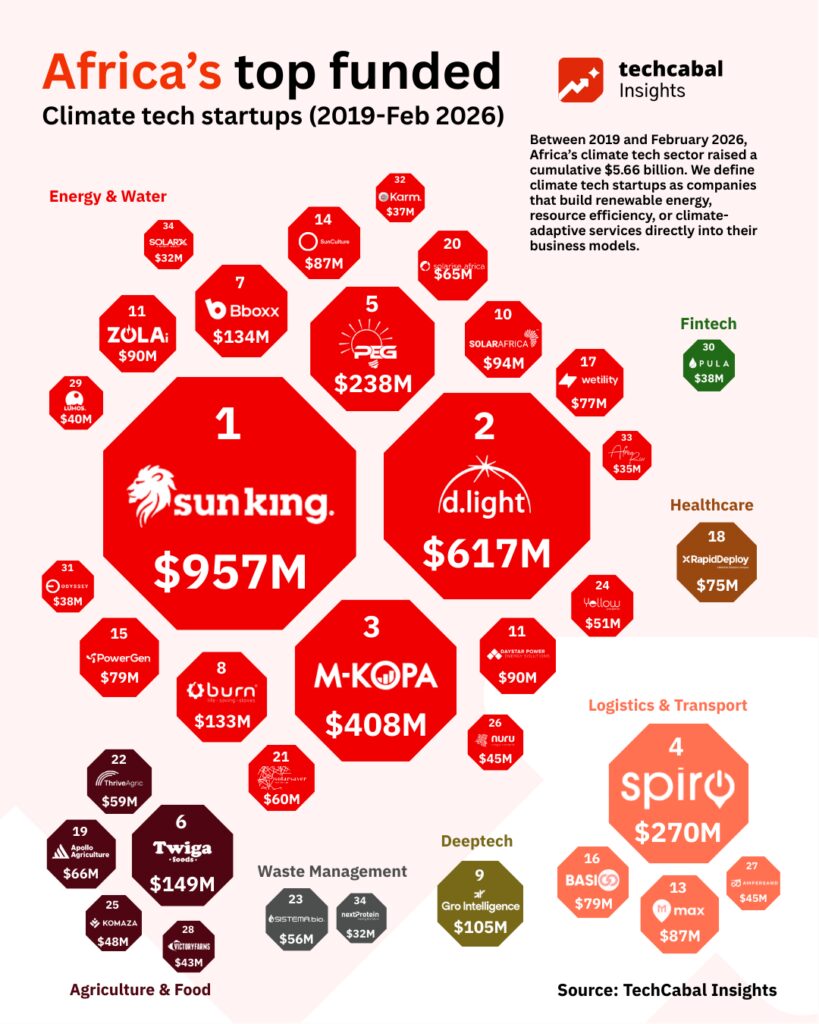

Five companies have raised ($2.49B) more than 40% of every dollar

Africa’s climate tech funding is highly concentrated at the top. The five top-funded startups -Sun King, d.light, M-KOPA, Spiro, and PEG Africa have collectively raised $2.49 billion, accounting for approximately 44% of all climate tech capital deployed on the continent since 2019.

All five share a common profile: asset-heavy business models, large consumer customer bases, and proven repayment track records that make them ideal vehicles for debt financing. Their dominance at the top of the capital stack reflects how DFIs and institutional lenders have learned to structure deals in this market.

Africa’s top funded climatetech startups (2019- Feb 2026)

Beyond the top five, the leaderboard remains predominantly an energy and e-mobility story. Of the top 15 startups by cumulative funding, 12 operate in solar, clean energy access, or electric mobility.

However, there are outliers in an otherwise energy-concentrated capital stack. They include two agriculture entries, Twiga Foods and Apollo Agriculture, and one climate services company (RapidDeploy).

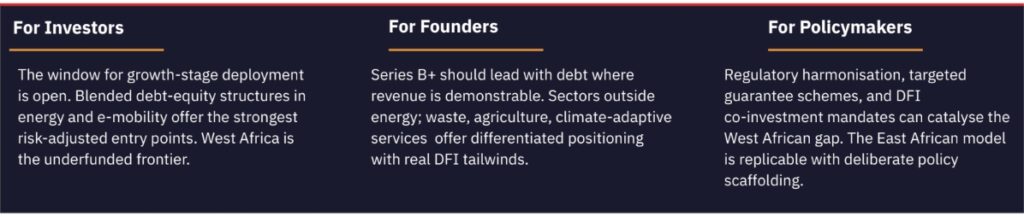

The signal for DFIs & policymakers:

The $191M raised by waste management and $86M by health-related climate tech startups represent serious underinvestment relative to their potential impact. Smallholder agriculture and informal waste sectors are disproportionately exposed to climate vulnerability, yet receive a fraction of the capital flowing to energy. Blended finance instruments designed specifically for these sectors could unlock a parallel capital mobilisation story.

What the Data Signals for 2026 and Beyond

Africa’s climate tech has hit a turning point. While the ‘funding winter’ slowed other sectors, climate tech reached a record $1.18 billion in 2025. The $201 million raised in early 2026 shows this wasn’t a one-time spike; the industry is now permanently operating at a much larger scale.

The question for every stakeholder in Africa’s green economy is not whether climatetech is a viable market. That question was answered in 2025. The question now is whether capital strategies, portfolio structures, and policy frameworks have caught up with what the data has been saying for years.

| Get exclusive research and data for Africa’s tech industry, with deep market intelligence, sector reports, and early access to new features. |

| Get exclusive research and data for Africa’s tech industry, with deep market intelligence, sector reports, and early access to new features. |