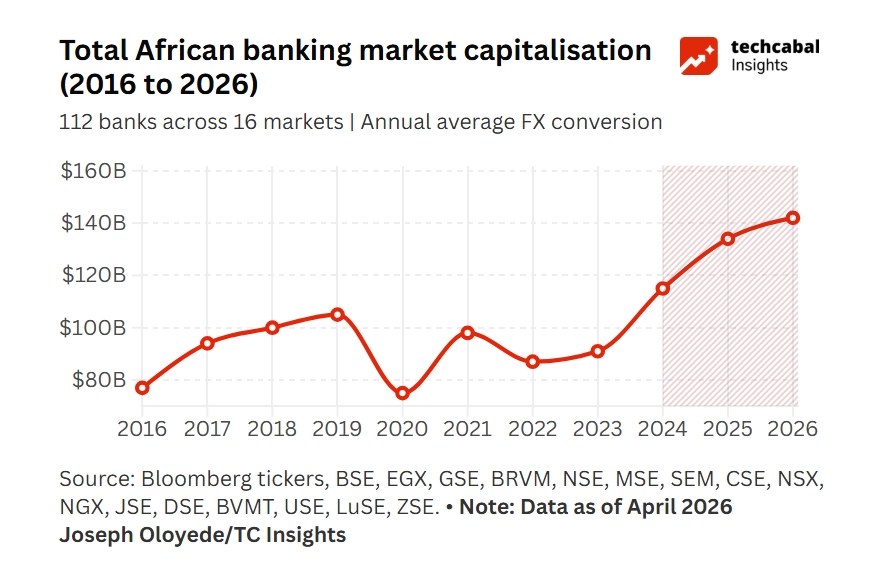

In 2016, the combined market capitalization of 112 listed commercial banks across 16 African countries stood at $77.5 billion. By 2026, that figure had grown to an estimated $142.3 billion. In the span of a single decade, Africa’s publicly listed banking sector grew by 84% in US dollar terms, a performance that outpaced many comparable regions when measured on a constant-currency basis.

Behind the headline number are more than a decade of policy decisions, currency swings, and technology investments that have collectively reshaped what African banking looks like.

A sharp contraction in 2020 pulled the aggregate to $75.9 billion as COVID-19 disrupted capital markets across the continent. A partial recovery in 2021 gave way to a further dip in 2022, largely driven by currency pressures in sub-Saharan Africa. The rebound from 2023 onward has added over $50 billion in aggregate market value in just three years, powered by recapitalisation drives, rising interest margins, and renewed investor confidence.

A continent, not a monolith

One of the most important facts embedded in the data is also the most commonly overlooked: Africa’s banking market is highly concentrated. South Africa, Morocco, Egypt, Nigeria, and Kenya collectively dominate the picture, accounting for the overwhelming majority of total market value. But their stories, and the forces shaping each, are strikingly different.

McKinsey’s March 2026 analysis of Africa’s banking sector confirms what the market cap data shows: approximately 70% of the sector’s revenues in 2024 were generated by the top five markets. South Africa alone accounts for more than a quarter of the continent’s banking output. The sector’s total market size reached around $107 billion in revenues in 2025, with double-digit growth in smaller markets signalling that new frontiers are opening.

Who is winning: The top five markets

Five markets account for the vast majority of Africa’s $142 billion banking sector by market cap. South Africa sits at the top, with four listed banks (Standard Bank, Absa, Nedbank, and Capitec) combining for $66.7 billion in 2026, a 47% share of the continental total.

Morocco comes second at $24.2 billion, representing 17%of the aggregate, its seven banks anchored by Attijariwafa Bank ($10.1 billion) and Banque Centrale Populaire ($6.5 billion). Egypt follows at $15.2 billion, an 11%share built largely on the performance of Commercial International Bank ($8.2 billion) and Faisal Islamic Bank ($1.5 billion).

Nigeria, despite the naira devaluation that compressed dollar valuations through 2023, holds $10.2 billion (7% of the total), led by GTCO ($2.5 billion) and Zenith Bank ($2.3 billion). Kenya rounds out the top five at $6.3 billion, with Equity Group ($2.3 billion) and KCB Group ($1.7 billion) as its two largest institutions. Together, these five markets represent roughly 85% of Africa’s total listed banking market cap, a concentration that has held firm across the entire decade.

African banking: A dynamic and evolving market

McKinsey’s analysis of Africa’s banking sector establishes a critical context for reading the market cap data. African banks delivered a return on equity of 19% in 2024 and 17% in 2025, well above the global average of 10%over the same period. This buoyant performance has been fuelled by elevated interest rates, growth in loan volumes, and significant profits from trading and foreign exchange activities.

The way banks generate revenue is also shifting. Despite consistently high interest rates over the last four years, growth from fees and services outpaced net interest income growth on the continent by 1.8 percentage points annually between 2020 and 2024. African banks are following the global pattern: non-interest revenue growing faster than traditional lending income, driven by digital payments, mobile banking, and fintech partnerships.

The top five markets account for approximately 70% of revenues, though double-digit growth in smaller markets signals that new frontiers are opening.

The continent’s cost-to-income ratio improved, reaching 49% in 2024 compared with the global average of 51.1%. However, this improvement is largely attributable to sustained revenue growth rather than increased cost efficiency. At 2.6%, the cost-to-asset ratio of African banks remained double the global average of 1.3%in 2024, indicating significant room for future operational efficiency gains.

In dollar terms, currency depreciation, inflation, and foreign exchange volatility weighed on performance across sub-Saharan Africa. On a fixed-currency basis, the continent’s banking sector expanded at a compound annual growth rate of approximately 17% between 2020 and 2024, compared with a global average of 7%. When measured in US dollars, revenues grew at a more modest 5.2 % CAGR from $81 billion to $99 billion over the same period, before accelerating to 7%in 2025 as macroeconomic conditions improved.

The fast risers

Beneath the five dominant markets, a set of smaller economies has delivered some of the most impressive growth trajectories in the dataset. These are markets where the absolute numbers remain modest, but the compound rates of expansion point to structural shifts in financial sector development.

Tanzania’s eight listed banks grew from $318 million in 2016 to an estimated $715 million in 2026, a 125% increase. CRDB Bank, the country’s largest listed institution, expanded from $161 million to $363 million over the period, while NMB Bank Tanzania grew from $129 million to $290 million. The Tanzanian banking sector has recorded a CAGR of 11.3%in revenues between 2019 and 2024, according to McKinsey’s analysis, one of the fastest among all African markets.

Zambia’s two listed banks, Zambia National Commercial Bank (ZANACO) and Standard Chartered Bank Zambia, grew from a combined $226 million in 2016 to $770 million in 2026, a 241%increase. Uganda’s three listed banks similarly expanded from $427 million to an estimated $1.0 billion, crossing the billion-dollar threshold for the first time. Malawi, despite being the dataset’s smallest market by total value, recorded a 305% increase across five banks, from $141 million to $572 million.

What is driving it

Three interlocking forces have driven the decade-long expansion in African banking market values: monetary policy, digital transformation, and rising financial inclusion. Understanding how these forces interact explains both the growth in aggregate market cap and the divergence between markets that have performed strongly and those that have faced headwinds.

- Interest rates and monetary policy: Across much of Africa, elevated interest rates have been the single most direct contributor to bank profitability over the past four years. High rates boost net interest margins, increase returns on government securities holdings, and have driven significant foreign exchange gains in markets that liberalised their currency regimes. Nigeria’s five largest banks recorded over $1.7 billion in foreign exchange gains in 2023 alone, representing approximately 40% of their total operating income. Egypt’s Monetary Policy Rate reached 27.5%in 2025, compressing borrowing for businesses but dramatically expanding lending margins for banks. The effect shows directly in McKinsey’s ROE data: African bank returns on equity soared from 9.0% in 2020 to 19.0% in 2024, nearly double the global average.

- Digital adoption and the payments revolution: Digital banking has moved from a differentiator to a baseline requirement across African markets. Payments grew at a CAGR of 8.0% in the retail segment between 2020 and 2024, making it one of the fastest-growing product categories in African banking. M-PESA in Kenya now serves more than 35 million active customers and has grown its contribution to Safaricom’s revenue from 31% in 2021 to 42%in 2025. In Nigeria, fintechs such as OPay have surpassed 50 million app downloads, while Moniepoint ranks among the leading merchant acquirers in the market. Traditional banks have responded with heavy investment in digital infrastructure, with several reporting tens of billions of naira per year in software and IT spending. This digital arms race has ultimately supported valuations by expanding the addressable customer base, particularly among previously unbanked populations.

- Financial inclusion as a structural driver: Africa has the world’s fastest-growing population, expanding by more than 2% each year between 2020 and 2025, with the continent’s working-age population increasing at almost 3% annually. This demographic tailwind is being converted into banking customers at an accelerating pace. Egypt’s financially included population reached 53.8 million out of 70.5 million citizens by June 2025. Digital lending in Kenya grew by 32% from 2020 to 2024, with demand for digital credit providers jumping fivefold between 2023 and September 2025. The SME segment, historically the most underserved, is projected to grow at 8% CAGR through 2030, the fastest of any segment in African banking.

What comes next: SMEs, AI, and consolidation

The decade-long growth in African banking market caps has been impressive. The next decade may be harder to navigate. As interest rate tailwinds fade, currency pressures persist in key sub-Saharan markets, and competition from fintechs and neobanks intensifies, the banks best positioned to sustain their valuations will be those that move beyond rate-driven profitability toward structural, capability-driven growth.

- The SME frontier: Small and medium enterprises represent the largest untapped growth opportunity in African banking. Across the continent, SMEs have historically been underserved: in Egypt, approximately 88% of SMEs remain unbanked, and SME banking credit represented only about 6.6% of GDP in 2022, compared with an average of about 20% in peer markets. McKinsey’s projections show the SME segment growing at a CAGR of 10.5% through 2030, the fastest of any product category in the lending market. Unlocking this will require a fundamental shift: from collateral-heavy credit assessments to data-driven underwriting using mobile money transaction histories, digital payment records, telecom usage patterns, and utility payments as proxy indicators of creditworthiness. Several banks are already moving. One Egyptian institution has built a dedicated digital SME lending platform offering instant approval and disbursement within 24 hours.

- Industrialising AI: Generative and agentic AI are projected to deliver productivity impact equivalent to $200 billion to $340 billion annually across the global banking sector, including a reduction of up to 20 percentage points in cost-to-income ratios from agentic AI deployments. African banks are at varying stages of this transition. South African incumbents have deployed AI in fraud detection, credit risk, customer service, and sales and marketing, and are now moving from fragmented pilots to enterprise-wide programmes. Moroccan banks are focused on automating the customer lifecycle, from onboarding and servicing through collections, while targeting instant processing for product approvals. Nigerian banks are investing in digital ecosystems designed to serve a population of which over 60% are under 25 and already online. The banks that industrialise AI fastest, without compromising data governance or regulatory compliance, will carry a structural cost advantage that compounds over time.

- Scale through consolidation: Regulatory pressure is accelerating consolidation across the continent’s banking sectors. In Nigeria, the Central Bank raised minimum capital requirements from $33 million to $330 million for international banks and from $16 million to $130 million for national banks, with a March 2026 deadline. In Kenya, new core capital requirements targeting 2029 are widely expected to reduce the number of independently viable institutions. Central banks in multiple markets are simultaneously tightening prudential standards and advancing open banking frameworks, a combination that rewards scale and penalises fragmentation. The merger of Unity Bank and Providus Bank in Nigeria and Nedbank’s announced offer to acquire a majority stake in Kenya’s NCBA Group are early signals of a consolidation wave that will likely reshape the continent’s banking landscape through the end of the decade.

The decade ahead will also be shaped by a two-speed macroeconomic reality. Countries such as Morocco have largely stabilised and avoided the worst of currency volatility, positioning their banking sectors for steady, efficiency-driven growth.

Sub-Saharan Africa, by contrast, continues to grapple with persistent inflation and currency pressure that weigh on dollar-denominated valuations even as local-currency performance remains strong. Banks that successfully price currency risk, diversify funding sources, and expand cross-border will be best placed to translate local profitability into durable, investable value.

When the total market cap of Africa’s listed commercial banks crossed the $100 billion threshold for the first time in 2018, it was a milestone with limited lasting significance: that figure would fall back below $90 billion within two years.

The crossing of $142 billion projected for 2026 feels different. It arrives on the back of recapitalisation, regulatory strengthening, accelerating digital adoption, and a continent that is, by every demographic measure, only becoming more financially active. The story of African banking’s first decade of data is one of real but volatile growth. The next chapter will be about making it stick.